CEC Trip to Canada

A China Entrepreneur Club (CEC) delegation will embark on an eight-day journey to Canada from October 16 to 23. This is the 9th destination country for CEC’s annual visits, following successful trips to the United States, UK, France, Belgium, Australia, Singapore, Germany, and Italy.

The journey will cover the cities of Montreal, Ottawa, Toronto, and Vancouver. Canadian Prime Minister Justin Trudeau will again meet with the CEC delegation, hosting them at the Willson House residence on Meech Lake. Just six weeks ago, Prime Minister Justin Trudeau met with CEC members at the China Entrepreneur Club Leaders Forum in Beijing during his first official visit to China. It created an opportunity for a candid discussion focused on the questions of China’s private sector business leaders concerning Canada-China business relations and partnership growth.

The delegation will mainly look into the policy landscape of Canada, the opportunities during economic transformation, competitiveness in talent and technology, and foster communication with important industries including technology and innovative industries, consumer goods, and finance.

CEC’s visit will include meetings organized by Power Corporation, Bombardier, Cirque du Soleil, and The Royal Bank of Canada. Roundtable dialogues will be held with the QG100 Network, the Toronto Financial Services Alliance (TFSA), the Canada China Business Council (CCBC), the Business Council of Canada (BCC) and the Asia Pacific Foundation of Canada.

– PRNewswire

China’s Slow but Assured Economic Rebalancing

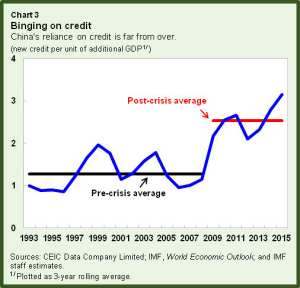

The rebalancing of China’s economy is a prolonged and sometimes tortuous process that is best described as “two steps forward, one step back”. In recent years, China’s cheap credit fueled ‘zombie’ state-owned enterprises (SOEs) have been amassing debt on a gargantuan scale pressing the International Monetary Fund (IMF) to issue a warning that the situation is “unsustainable” By some estimates, China’s corporate debt stands at US$18 trillion, equivalent to about 169% of GDP which, although average for a developing economy, is still extremely high by any measure.

Markus Rodlauer, deputy director of the IMF’s Asia-and Pacific Department, told the Telegraph newspaper in early October that “the level of financial and corporate debt and the complexity of the financial system and rapid growth in shadow banking is on an unsustainable path…The longer it lasts…the more serious the disturbance and the disruption might be…While still manageable in its size given the size of the public assets under public control, the trend is dangerous…”

Just as the IMF warning made headlines and despite a 10% dip in China’s exports last month reflecting the fragility of global demand, it was reported that China’s overall share of global exports in 2015 actually climbed to 14.6% from 12.9% a year earlier. This is the highest proportion of world exports ever reported in IMF data going back to 1980. This rise in global export share behooves China naysayers to admit that the manufacturing slice of China’s economy is really declining with the void being filled increasingly by services and consumption as the new drivers of growth.

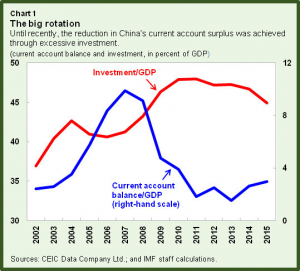

Longmei Zhang, an economist in the same department at the IMF, writing recently in IMFdirect, used the analogy of a high-powered and fast-sailing ship that nonetheless is listing and drawing some water to describe the current state of structural reform in China. The country has been trying to make the voyage more smoother and balanced and growth more sustainable in four interrelated dimensions’ – external, internal, environmental and distributional. Since the 2008 global financial crisis, she said China has made “mixed-strong’ progress in terms of external balancing, i.e., switching from external to domestic demand and services, but has a somewhat uneven track record in the other dimensions.

Until 2011, the reduction in the external imbalance was reflected in a growing internal imbalance in terms of the rising levels of investment to GDP ratio due to strong fiscal stimulus. Since 2012, however, some headway has been made away from state-led investment to consumption, both private and state, and from manufacturing to services, with a major bounce in 2015. Consumption now contributes more than 2/3 of GDP growth.

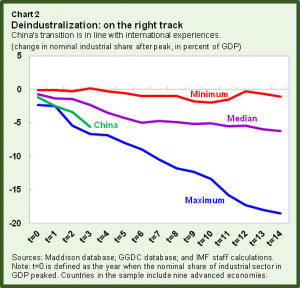

At the same time, however, surging credit usage has become China’s Achilles heel with credit intensity, the amount of new lending provided for each additional unit of output, more than doubling since the global financial meltdown. In addition, while energy intensity of industry has fallen, air pollution remains stubbornly serious as is income inequality even though labour’s share of GDP has steadily grown.

This week, in its marathon bid to rein in high levels of corporate debt, the government announced a set of guidelines that includes encouraging mergers and acquisitions, bankruptcies, debt-to-equity swaps, and debt securitization. The National Development and Reform Commission (NDRC) emphasized only companies with “good prospects” will be allowed to negotiate swaps with lenders. To date, only a handful of insolvent companies have been given the go-ahead to do debt swaps. In recent years, the Chinese authorities have pledged to introduce more market competitive mechanisms into the lumbering SOE sector and shut down ‘zombie companies’ that are kept alive through easy loans from state banks.

Lian Weiliang, deputy chairman of the NDRC told reporters, “market-oriented debt conversion is by no means a free lunch. The relevant market players will make their own decisions, take their own risks and enjoy the benefits. The government takes no responsibility for bailing out losses.”

The government will combine deleveraging with over-capacity reductions and provide preferential tax relief for firms to cut debt levels. As well, the People’s Bank of China (PBoC), China’s central bank, will adopt favourable monetary policies as it pushes banks to transfer bad loans to asset management companies and encourage securitization of bad assets. As this policy package was announced, the central government also resolved to improve market access for foreign companies. In the future, with the exception of certain sensitive industries that are strictly off-limits, foreign investment would only require registration as opposed to approval.

In the backdrop of the recent economic rebound, analysts at US investment bank Morgan Stanley revised their forecast of China’s GDP growth this year to 6.7% from 6.4% and 6.4% from 6.2% for 2017. Moreover, Bloomberg’s survey of 58 economists at the end of September also pegged their expectations at 6.6%, reflecting growing optimism among foreign analysts. In this respect, China must maintain +6% growth to the end of the decade if it wishes to double incomes to US$10,000 by that time. By this writer’s calculation, average incomes should reach $11,000 by end 2020 if the economy can maintain 6.5% growth throughout the decade.

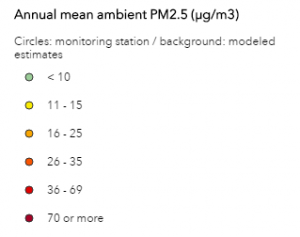

China’s Air Still Among the Worst But Canada Among the Best: WHO air quality model

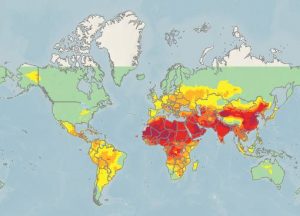

A new WHO air quality model confirms that 92% of the world’s population lives in places where air quality levels exceed WHO limits. Information is presented via interactive maps, highlighting areas within countries that exceed WHO limits.

It also represents the most detailed outdoor (or ambient) air pollution-related health data, by country, ever reported by WHO. The model is based on data derived from satellite measurements, air transport models and ground station monitors for more than 3000 locations, both rural and urban. It was developed by WHO in collaboration with the University of Bath, United Kingdom.

“WHO’s Ambient Air quality guidelines” for annual mean of particulate matter with a diameter of less than 2.5 micrometres (PM2.5) are 10 μg/m3 annual mean. PM2.5 includes pollutants such as sulfate, nitrates and black carbon, which penetrate deep into the lungs and in the cardiovascular system, posing the greatest risks to human health.

Toronto to Host the Largest Ever Travel Delegation from China to Canada

Toronto will host the largest travel delegation ever to come from China to Canada. The Chinese incentive travel group, NU Skin Greater China, will send 6,000 of its elite salespeople to Toronto in 2018, following a signing ceremony held this week in Shanghai between NU Skin officials, Tourism Toronto and the Ontario Minister of International Trade. This travel program is estimated to generate $8.3 million in visitor spending in Ontario.

This coveted win is part of Tourism Toronto’s multi-year strategy to attract both leisure and corporate travellers from China, which remains the largest overseas market for tourism. In 2015 alone, 260,000 visitors arrived from China, a figure that has doubled since 2010.

– PRNewswire

China’s Burgeoning Middle Class Spending

Unbeknownst to the average North American reader, China’s transition to a consumption-led economy has been going on for years. This has led to the burgeoning of a middle class that is progressively cosmopolitan and happier to part ways with hard earned cash in contrast to the previous thrifty and savings-obsessed generation.

Defining China’s middle class as urbanites earning US$9,000 to $34,0000 a year, management consultancy McKinsey and Co. recently projected it will account for 76% of the country’s urban population by 2022, a massive expansion from the tiny 4% in 2000. Last year, China’s urban population approached 730 million or a little over 54% of the entire population which is estimated to expand by one percentage point a year through the 2030s. Even if China’s cities stopped growing, the middle class would still equal 550 million people in seven years, almost 3.75 times America’s whole working population.

More important, the middle class in China is becoming richer in comparison to stagnant middle class incomes in the US and other Western countries. In 2012, China’s “mass” middle class earned $9,000 and $16,000 but within a decade from that date, 54% of Chinese urbanites will be considered “upper middle” class, earning $16,000 to $34,000 a year. That might seem miniscule compared to upper middle class incomes in the US, but adjusted for purchasing power parity (PPP), it means a major jolt in consumer spending.

In a similar analysis, the Boston Consulting Group projected Chinese consumption to grow 9% a year until at least 2020 and China’s consumer economy as a whole by 55% to $6.5 trillion from $4.2 trillion last year, based on the conservative setting of China’s GDP growth at 5.5% per annum even though this year’s growth is expected to fall within 6.5% to 6.7%. In addition, Chinese household debt-to-GDP ratio is less than half of US households that currently stands at around 40%. Not only does this mean Chinese consumers spend far less on servicing debts but also that they’re able to take on more debt, if they choose to do so. Culturally and traditionally, however, Chinese families possess a deep aversion to bank debt, preferring to purchase cars, homes, children’s education, and other major outlays with cash or money borrowed from relatives.

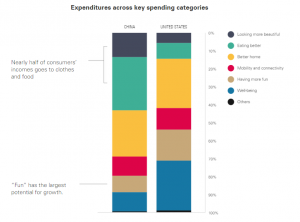

A Goldman Sachs report a year ago described the changing patterns of spending among Chinese consumers. Currently, Chinese families spend on average $7 a day, half on food, compared to $97 a day in the US but as disposable incomes rise, Chinese families will spend more on eating better, dressing nicer, living more comfortably, using more smartphones and cars, having more fun, and spending more on well-being, health, and children’s education. While Chinese consumers prefer to spend more on clothes and food, Goldman Sachs expects them to dig into their pockets for more ‘fun’ – going on vacations at home and abroad, dining out more, and seeking more entertainment and cultural attractions. Currently, Americans spend some 17% of their disposable incomes on having fun whereas Chinese splurge only 9%.

One conspicuously spendthrift group is China’s millennials, those born in the mid-1980s and after. They take trips overseas on a whim, buy stuff more impulsively, and hardly saves at all, much to the chagrin of their parents. A contributor to Forbes magazine writes Chinese millennials are able to keep up their spend-happy ways due to two factors that make their American counterparts envious. First, they are not encumbered by massive student loan debts plus compound interest which American millennials often take decades to pay back, if they haven’t declared bankruptcy already. Chinese millennials enjoy the luxury of their parents paying for their educations which according to Tuition.io averages around $2,200 per year, substantially less than in the US and affordable for most families. In the US, there is a whopping $1.3 trillion in outstanding student loans and more than seven million borrowers in default with tens of millions more struggling to repay.

Second, closely linked to their aversion to household debt coupled with the lack of investment options, Chinese families often plough their funds into acquiring homes with many owing multiple properties that explains to a large extent China’s inability to rein in real estate bubbles across the country. Looking out for their offspring, Chinese parents often hand over an extra apartment that saves millennials immense costs associated with securing a home on their own. By comparison, in the US, millennials, already loaded down with student loans, can hardly afford to rent decent apartments, let alone considering to buy a home. This also explains why millennials in the West travel less and spend far less on the trips they do take than their Chinese counterparts.

By 2020, Chinese millennials will top 300 million (compared to 80 million in the US) who, unlike their parents that are fixated with famous brands and acquiring properties, will form the second generation of Chinese consumers. This group desires to be more spiritually and culturally fulfilled, venturing overseas to expand their horizons and living for the moment. While many will still follow the crowd on group tours, the adventurous minority will want more individualized experiences, preferring to explore sites off the beaten path. And many will continue to indulge in luxuries while others focus on family and children, less burdened by mortgages and car loans like their Western brethren.

Not to be forgotten, a final mainstay of China’s consuming horde is the increasing legions of the elderly. Another recent study by McKinsey & Co. builds on the findings of a previous analysis in 2011 (here I focus on the elderly). The authors state that five years ago, they had grossly underestimated the speed and force of spending by the Chinese elderly. Much of what they had anticipated would happen in 2020 already started happening in 2015. 52% of the 55-65 age group expressed preference for premium products as compared to 32% in 2012 and constituted the group most likely to trade up in their buying habits. They no longer shun famous brands, do not shy away from indulgences, and have grown more accustomed to researching their purchases online.

The Chinese middle class has come into its own and we’re witnessing only the start of China’s ever expansive, changing, and increasingly sophisticated consumption trends that bode well for major surges in imports from abroad.